Why Is Personal Finance Dependent Upon Your Behavior? A Detailed Guide to Financial Success

Introduction

Personal finance is often reduced to a set of rules: save aggressively, invest wisely, and spend cautiously. However, the real truth is that what you do with your time and money boils down to more than just hard-and-fast principles. There are many ways to optimise how money flows through your pockets to some extent, but nothing has anywhere close to the impact that your personal financial behaviour does. When it comes to your finances, whether you are budgeting, saving or investing, the habits and decisions you make daily have an impact on your financial future.

Studies in behavioural finance suggest our psychological tendencies, emotions and social pressures affect the way we deal with money, which can sometimes cause us to make decisions that don’t jibe with our best financial interests. In this article, we’ll cover what makes up personal finance and how it’s tied to your behaviour with practical examples, science-backed conclusions, and actionable strategies that you can use to take control of your finances.

You’ll want to identify and challenge whether or not the changes you would make that lead to wealth generation are attainable for you, but by knowing what your financial habits look like, you can build a plan based around creating wealth that many people never have a chance to create because of money mistakes. So, let’s get going on how personal finance behaviour forms your financial fate.

Section 1: The Psychology Behind Personal Finance

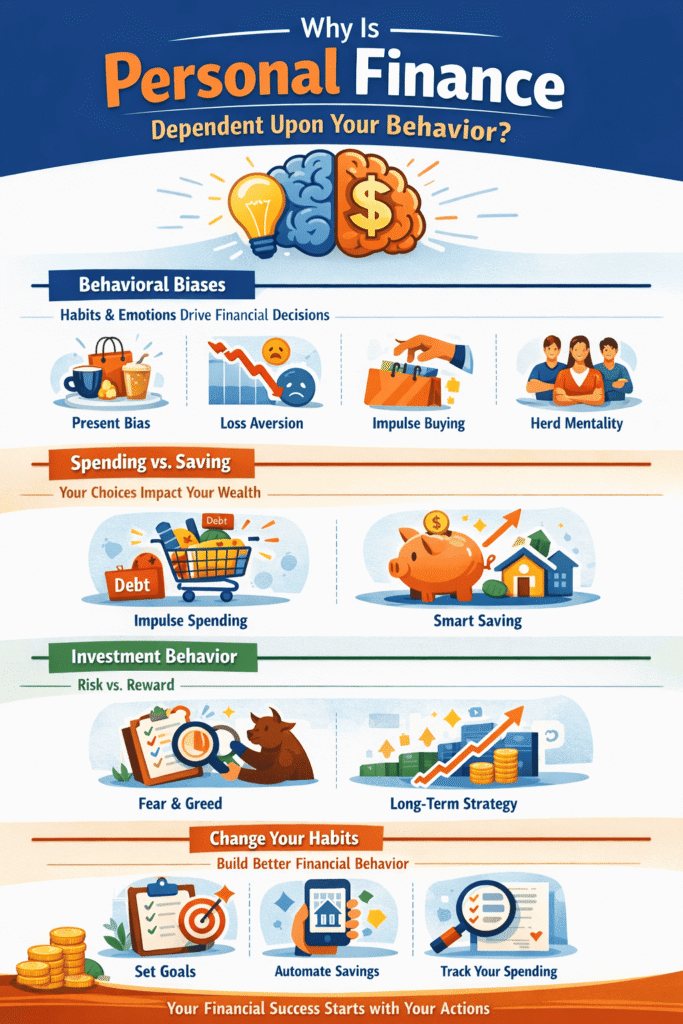

How Behavioural Biases Influence Financial Decisions

One of the key reasons personal finance is so behaviour-dependent is because of the biases and mental shortcuts we use when making money decisions. These biases often cloud our judgment, leading to poor financial choices. Here are some of the most common biases:

- Present Bias: We tend to prioritise immediate rewards over future gains, which makes saving and investing for the future difficult. For example, you might choose to buy something now instead of saving for retirement.

- Loss Aversion: We fear losing money more than we enjoy gaining it, causing us to avoid risk in investing or hold onto losing investments out of fear of realising a loss.

- Example: Keeping a stock that has performed poorly because you don’t want to admit the loss.

- Confirmation Bias: We tend to seek information that supports our existing beliefs, often ignoring sound financial advice. This leads to poor investment decisions or sticking to outdated financial habits.

- Example: Only listening to financial advice that supports your idea of real estate investment, even when it may not be the best option for you.

Interactive Element:

- Test Your Biases: Take this quick quiz to see if you have any of these biases that could be affecting your financial decisions.

How Spending and Saving Habits Impact Your Financial Success

The Role of Daily Spending Habits

It’s easy to assume that a high salary automatically leads to wealth, but the truth is, how you spend your money has a greater impact on your financial health. Behavioural psychology shows that spending habits are often influenced by emotions, peer pressure, and instant gratification.

- Impulse Purchases: Emotional or spur-of-the-moment buys can derail your financial goals, especially when they accumulate.

- Example: Walking past a store, seeing a sale, and buying something you don’t need.

- Status Spending: The desire to “keep up with the Joneses” can lead to overspending on luxuries, even if it doesn’t align with your long-term financial plans.

Example

Buying an expensive car because of social pressure, despite having student loan debt

Saving for the Future: The Challenge of Building Wealth

To build wealth, you need consistent saving and long-term thinking but many people fail at this due to a lack of discipline and the influence of behavioural biases. Without automation, it’s easy to let savings slide and prioritise short-term pleasures over long-term financial security.

- Building an Emergency Fund: Behavioural finance experts recommend automating savings to ensure consistency.

- Example: Setting up automatic transfers into a high-interest savings account as soon as you receive your paycheck.

- Setting Realistic Goals: Defining clear financial goals (e.g., “I’ll save $500 per month for my emergency fund”) and sticking to them helps overcome the temptation to spend.

Interactive Element: Use this savings calculator to see how small, regular deposits can grow into a significant emergency fund.

Section 3: Behavioural Patterns in Investing

Investing and Risk Management: A Behavioural Approach

Investing isn’t just about choosing the right stocks or bonds it’s about managing risk and behavioral tendencies. A rational approach to investing requires a long-term mindset, but psychological biases like overconfidence and herding behavior can lead to poor decision-making.

- Overconfidence Bias: Many investors think they can outsmart the market, leading them to take excessive risks.

- Herding Behavior: The fear of missing out (FOMO) drives many people to follow the crowd into risky investments (e.g., jumping into the market during a bubble).

Example: Relying on day trading or speculative stocks without understanding the full risks.

Example: The dot-com bubble and the cryptocurrency boom both saw many investors chasing trends, only to suffer major losses later.

Interactive Element: Investment Risk Assessment Tool

Take this tool to find out how much risk you’re comfortable with and tailor your portfolio accordingly.

Developing a Mindful Investment Strategy

One of the most important aspects of financial success is developing an investment strategy that’s in line with your goals and risk tolerance. Behavioral finance experts recommend:

- Diversifying your portfolio to minimize risk

- Avoiding emotional decision-making in the face of market volatility

Section 4: Changing Your Financial Behavior for Success

Steps to Improve Your Financial Behavior

- Identify Behavioral Triggers: Recognize what causes impulse spending or emotional decision-making and work to minimize these triggers.

- Example: Avoiding the temptation to shop by leaving your credit card at home or using cash for discretionary spending.

- Use Behavioral Tools: Use apps and tools that help you stay on track with saving, investing, and budgeting. Automation is a key strategy for overcoming behavioral biases.

- Example: Use apps like Mint, YNAB, or Acorns to automatically track and save money.

- Reframe Your Financial Mindset: Shift from a scarcity mindset (where you fear not having enough) to an abundance mindset, where you focus on growth and opportunity.

- Pro Tip: Instead of thinking, “I can’t afford this,” reframe to, “What can I do to afford this in the future?”

Behavioral Finance: The Key to Financial Freedom

By changing your financial behavior setting clear goals, developing a mindful approach to spending, and using psychology-based tools you can create a solid path to financial security and wealth-building.

Conclusion

Personal finance is not just about the numbers, it’s about how you behave with money. Whether it’s your spending, saving, investing or planning for retirement, the decisions you make each day are dictated by your financial habits and psychological biases. Knowledge of these behaviors might help you to make improved financial decisions, and build long-term wealth.

The big lesson is that personal finance success comes from aligning your actions with your goals, and taking advantage of what you know about behavioral finance to make wiser choices.

Call to Action:

Want to improve your financial behavior? Start by setting a realistic financial goal today and automate your savings!

How does behavior impact personal finance?

Behavior influences key financial decisions like spending, saving, and investing. Psychological biases, emotional spending, and habits shape how you manage money.

What are the most common financial behavior biases?

Common biases include present bias (prioritizing immediate gratification), loss aversion (fear of losing money), and confirmation bias (seeking info that confirms existing beliefs).

How can I change my financial habits for better results?

Start by tracking your spending, setting clear financial goals, and automating savings. Overcoming emotional triggers and sticking to a budget can lead to better financial decisions.

Why do people struggle to save money despite knowing its importance?

Emotional spending, lack of immediate rewards from saving, and behavioral biases like present bias prevent people from consistently saving for long-term goals.

What role does mindset play in personal finance?

Your mindset determines how you approach money. A growth mindset helps you focus on opportunities for wealth-building, while a scarcity mindset may lead to financial anxiety and poor choices.